September 20, 2024—Since March 2022, we’ve been in the midst of a Fed rate ‘tightening cycle’—it seems like SO long ago we enjoyed mortgage interest rates that, for many, were the lowest we’ve seen in our lifetime. At the same time, though, the Fed has been raising rates to tame inflation, which might also be the highest we’ve seen in our lifetime.

Thankfully, we are seeing the light at the end of the tunnel: Federal Reserve Chairman Jerome Powell hinted that the Fed could cut rates in September. In fact, as of the date of this writing, the Fed has just cut rates by 50bps.

So, let’s unpack this: What does this ‘rate cut cycle’ mean, and what should we do next?

WHAT IT MEANS

- It’s NOT a mortgage rate cut: When we talk about a ‘rate cut,’ we’re referring to the benchmark interest rate, which is set by the Fed. This does NOT indicate that mortgage rates will drop. In fact, mortgage rate trends will have already adjusted by the time the cut actually happens. What’s as important is the language of the Fed statement and Jerome Powell’s press conference that follows.

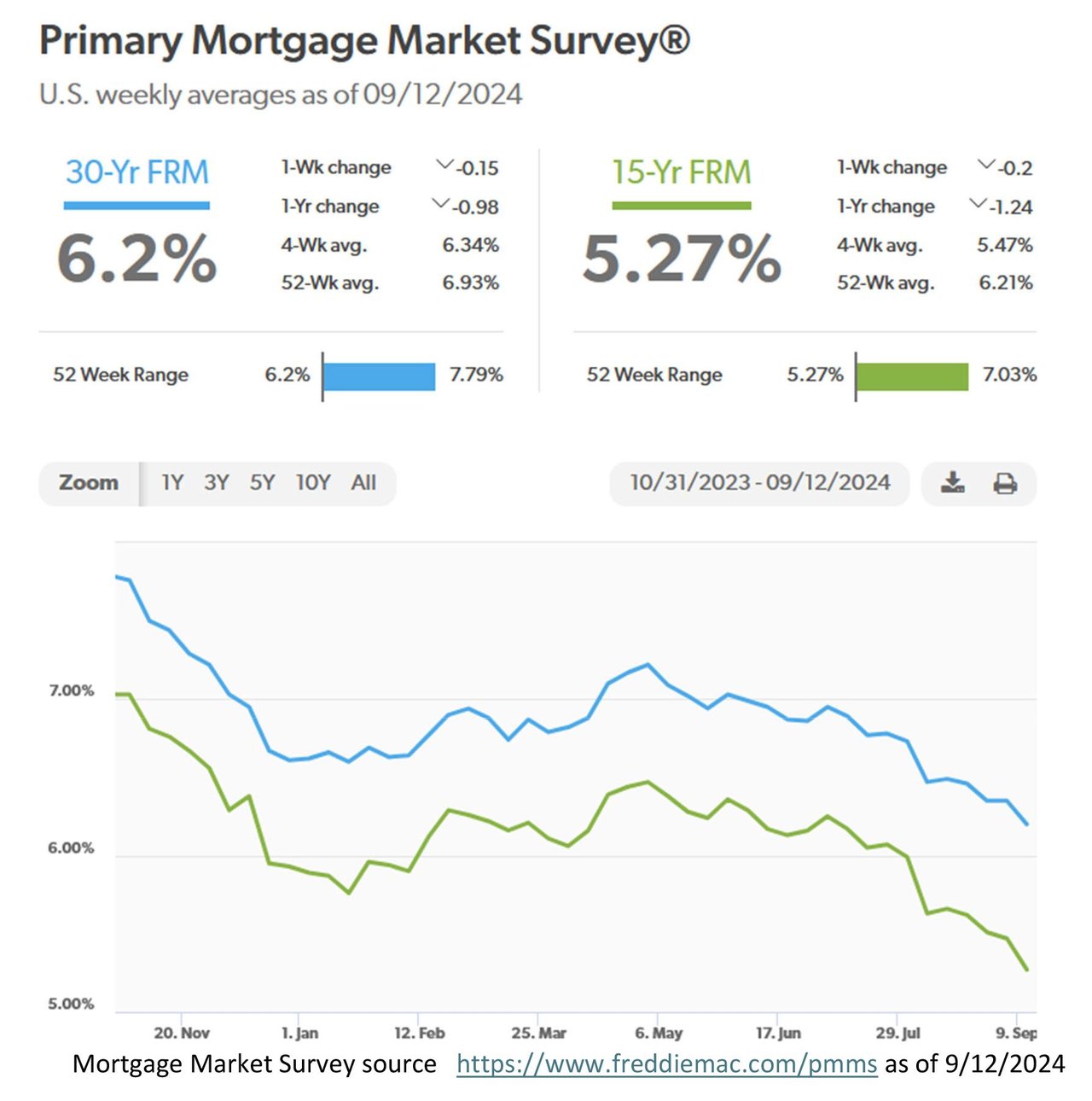

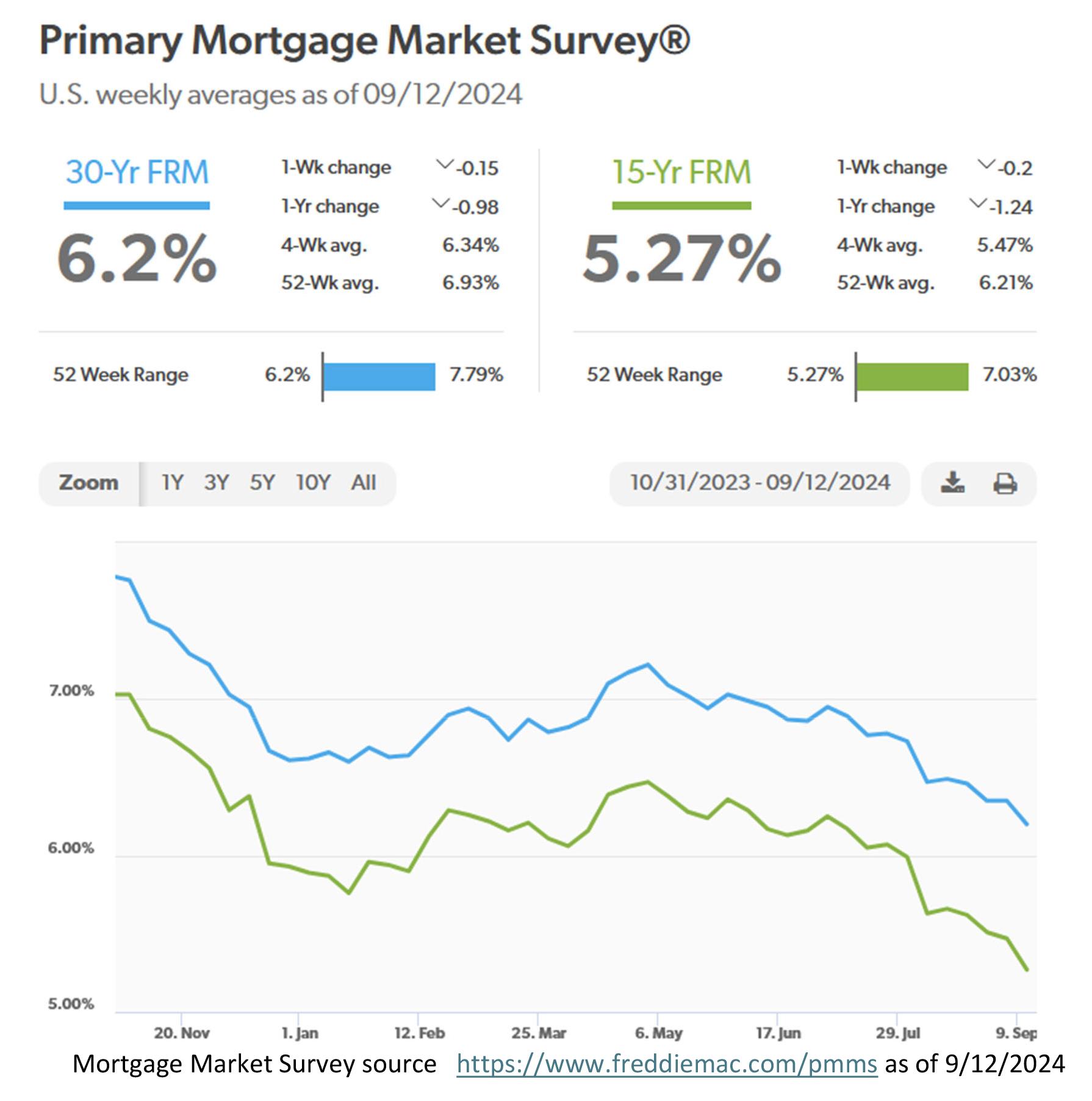

- Mortgage rates are already trending lower: After the Fed Chairman hinted at the rate cut, the bond market, and subsequently mortgage rates, reacted. Following the message, they dropped to two-week lows, and it’s likely they’ll continue trending lower leading up to the official rate cut, unless the Fed changes its tune. Take a look at the mortgage rate chart from FreddieMac below for example. Showing how mortgage rates like an escalator are trending downwards – just not in a straight line.

- Competition could heat up: With rates trending lower and the fall fast approaching, many buyers could be preparing to make a move before the winter. With inventory still limited, this could cause more competition.

WHAT TO DO NEXT:

- Consider a rate lock: Wait, rates are trending down you said now why would I lock my rate? Good question. In the past 20 years I’ve been originating mortgages, I’ve seen the market emotionally react and the desired rate disappear in a matter of minutes. Though we watch the market, locking the rate will protect you just in case rates bump higher before you close on a loan. If rates go lower, some loans have a ‘float down’ option that allows a lower rate. Best not to gamble and lose out.

- Set your ‘strike’ price: Now this is key. Many have been waiting for mortgage rates to drop, feeling they’ll refinance. Now’s the time to know your strike price, meaning know in advance the exact rate you need to hit that the math tells you it makes sense to refinance. Don’t guess. Mortgages are financial instruments – make a tactical decision and act on that plan.

- Prepare your paperwork: If you’re waiting to buy or refinance until after the Fed’s decisions, make sure you have everything else in line so you can jump when it’s time (preapproval, disclosures, W2s etc.) If you don’t know what you need to do to prepare – no problem – ask me!

The Fed rate cuts have been anticipated for some time and that time is now upon us. As a result, this escalator ride downward in mortgage interest rates is a time of lowering barriers – lowering the buyer affordability barrier to buy and a seller reluctance to sell. All in all, it does seem like Fall of 2024 is shaping up to be a time of change. And we’ll be ready.

Mortgage Market Survey source https://www.freddiemac.com/pmms as of 9/12/2024

NMLS# 459793 | BRANCH NMLS# 2475579 | CORPORATE NMLS# 1820