Buying in Flood Zones

Authored by Laurel Housh, Regional AVP of Disclosure Source NHD

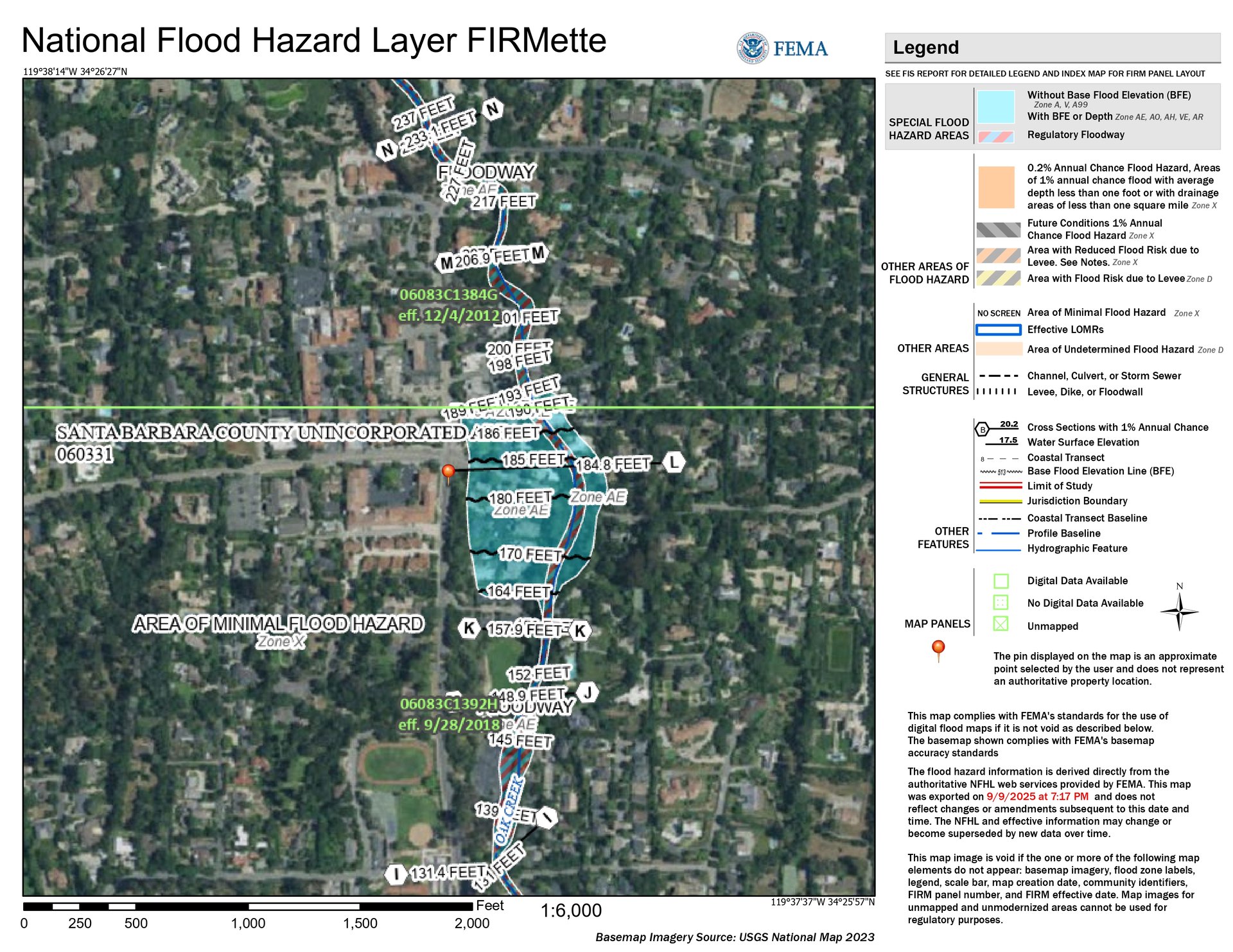

In Santa Barbara and Montecito, all properties carry some measure of risk, and it’s critical to identify those affecting your potential purchase. Flood zones are an important consideration for real estate, influencing property values, insurance requirements, and financing options. With coastal areas, creeks, and canyon terrain, certain properties face a higher risk, making it essential for buyers and sellers to understand Federal Emergency Management Agency (FEMA) flood zone classifications and their implications. Historical events, such as the 2018 Montecito debris flows, underscore the importance of evaluating flood risk when making property decisions.

FEMA flood zone map of Montecito, California, highlighting areas with higher flood risk.

Buying a home in a flood zone requires careful consideration and research to ensure you're aware of the risks and financial implications. Here's a comprehensive overview of what you need to know:

1. Understand Flood Zone Classifications

The Federal Emergency Management Agency (FEMA) creates and updates Flood Insurance Rate Maps (FIRMs) that classify areas based on their flood risk. These maps are crucial for determining a property's flood risk and insurance requirements.

-

High-Risk Zones (Special Flood Hazard Areas - SFHAs): These zones have a 1% or greater chance of flooding in any given year. For a 30-year mortgage, there's at least a 1 in 4 chance of flooding.

-

Zone A: Areas with a 1% annual chance of flooding, but without a determined base flood elevation.

-

Zone AE: Same as Zone A, but with a determined base flood elevation.

-

Zone V and VE: Coastal areas with additional hazards from storm-induced waves.

-

Moderate to Low-Risk Zones: These areas are outside the SFHA.

-

Zone X, B, and C: Areas with a 0.2% annual chance of flooding (the "500-year floodplain"). While insurance isn't typically required, a significant number of flood insurance claims come from these zones.

2. Flood Insurance is a Must-Have (and Often Required)

Standard homeowners’ insurance policies do not cover flood damage. You need a separate flood insurance policy.

-

Lender Requirements: If you are buying a home in a high-risk flood zone (Zone A or V) with a mortgage from a federally regulated or insured lender, flood insurance is mandatory. Your lender will perform a flood determination to verify the property's flood zone status.

-

National Flood Insurance Program (NFIP): Most flood insurance policies are provided through the NFIP, a federal program managed by FEMA. The National Flood Insurance Program offers coverage for the building itself (up to $250,000) and personal property (up to $100,000). If you believe repairs could exceed $250,000, you may want to consider a supplemental policy from a private insurer.

-

The 30-Day Waiting Period: Be aware that there is typically a 30-day waiting period for a new flood insurance policy to take effect. However, if the policy is required for a mortgage, it will take effect immediately upon closing.

3. Factor in the Cost

Flood insurance can be a significant and ongoing expense. The cost varies widely based on:

-

Flood Zone: Premiums are higher in high-risk zones.

-

Home's Elevation: The elevation of your home relative to the base flood elevation (BFE) is a major factor. A higher elevation property may carry less risk, which can lead to a lower premium. You may need an Elevation Certificate to get an accurate quote.

-

Age and Construction: The age and type of construction of your home will also influence the premium.

4. Investigate the Property's Flood History

FEMA maps are a great starting point, but they are not the only thing you should consider. Some maps may be decades old.

-

Seller Disclosure: Inquire directly with the seller about any past flood damage. Be aware that disclosure laws vary by state, and some sellers are not legally required to provide this information.

-

Real Estate Agent: Your real estate agent can help you learn more about the property's history and potential flood risks.

-

Home Inspections: Consider hiring professionals who specialize[s] in flood-related risks, detecting water damage and related issues.

5. Research Local and Community Flood Management

-

Local Ordinances: Check with the local city or county department of watershed management to understand any local flood management ordinances or building codes.

-

Community Rating System (CRS): Some communities participate in the CRS, which incentivizes them to go above and beyond minimum NFIP requirements. This can result in a discount on flood insurance premiums for residents.

6. Consider Mitigation Measures

If you decide to buy in a flood zone, you can take steps to reduce your flood risk and potentially lower your insurance premiums.

- Elevate Key Systems: Elevate your furnace, water heater, and electrical panels.

- Improve Drainage: Ensure the ground around your house slopes away from the foundation.

- Install Check Valves: Install check valves in your plumbing to prevent floodwater from backing up into your drains.

Learn More from an Industry Expert

With her expertise at Disclosure Source NHD, Laurel Housh provides valuable insights that help buyers and sellers understand risks, insurance requirements, and disclosure obligations. To continue sharing her knowledge, Laurel also conducts webinars on topics like flood zones, fire zones, and other natural hazards, providing opportunities for real estate professionals and homeowners to learn directly from an industry expert. Informed homeowners and buyers in Santa Barbara and Montecito can use a solid understanding of flood zones to avoid surprises with insurance and financing, and potentially get a better buy on a home with manageable flood risks.